Boost Profits with Financial Forecasting

Navigating the complexities of the modern business landscape demands more than just reacting to present circumstances; it requires a proactive approach rooted in foresight. This is precisely where financial forecasting emerges as an indispensable tool for businesses of all sizes. It’s the art and science of estimating future financial outcomes based on historical data, current trends, and projected events. By meticulously analyzing past performance and considering potential shifts in market conditions, economic factors, and internal operations, companies can build a clearer picture of what lies ahead, transforming uncertainty into actionable insights.

The ability to accurately predict revenue, expenses, and cash flow is not merely an accounting exercise; it's a strategic imperative. Without a robust understanding of future financial positions, businesses operate in a reactive mode, making decisions based on assumptions rather than data-driven projections. This lack of foresight can lead to missed opportunities, inefficient resource allocation, cash flow crises, and ultimately, a significant drag on profitability.

Effective financial forecasting empowers leaders to make informed decisions, whether it’s planning for expansion, managing inventory, hiring new talent, or seeking investment. It provides a roadmap that helps align operational activities with strategic goals, ensuring that every department contributes to the overarching financial health of the organization. Moreover, it serves as an early warning system, highlighting potential financial bottlenecks before they become critical issues, allowing management to implement corrective measures proactively.

Ultimately, the power of a well-executed financial forecast lies in its capacity to transform a company’s financial trajectory. It enables businesses to optimize resource utilization, identify areas for cost reduction, capitalize on growth opportunities, and mitigate risks. The journey toward enhanced profitability and sustainable growth begins with a commitment to understanding and mastering the principles of robust financial forecasting.

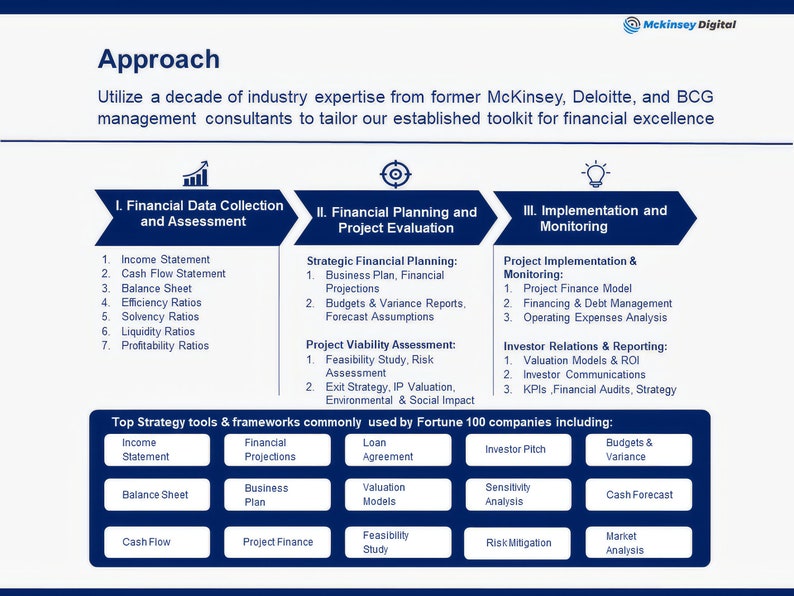

What is Financial Forecasting and Why Does It Matter?

![]()

Financial forecasting is the process of estimating the financial outcomes of an organization for a future period. It involves predicting revenues, costs, and profits, as well as cash flows, balance sheet items, and other financial metrics. The core purpose is to provide management with a clearer understanding of potential future financial performance, enabling them to make better decisions in the present. It’s not about absolute certainty, but rather about creating a probable range of outcomes based on available data and assumptions.

The significance of financial forecasting cannot be overstated in today's dynamic business environment. Firstly, it forms the bedrock for strategic planning. Businesses need forecasts to set realistic goals, allocate budgets effectively, and plan for future investments or divestitures. Without a reliable forecast, strategic initiatives might be based on guesswork, leading to suboptimal outcomes. Secondly, it plays a critical role in budgeting. A forecast provides the quantitative basis for setting departmental budgets, ensuring that resources are aligned with expected revenues and operational needs. This prevents overspending or underspending, both of which can impact profitability.

Furthermore, financial forecasting is vital for cash flow management. Predicting when cash will come in and go out allows businesses to avoid liquidity crises, manage working capital efficiently, and identify periods of surplus cash that can be invested. It also aids in performance measurement. Actual results can be compared against forecasted figures to assess the accuracy of predictions and the effectiveness of strategies. This variance analysis provides valuable insights into operational efficiency and market responsiveness. Lastly, robust financial forecasts are often a prerequisite for securing financing or attracting investors. Lenders and investors rely heavily on a company's projected financial health to assess risk and potential returns, making a compelling forecast an essential component of any funding proposal.

The Role of Assumptions in Forecasting

It's crucial to understand that all financial forecasts are built upon a set of assumptions. These can range from internal factors like pricing strategies, production volumes, and staffing levels, to external factors such as economic growth, competitor actions, interest rates, and consumer spending habits. The quality and realism of these assumptions directly impact the accuracy and reliability of the forecast. Therefore, a key part of the forecasting process involves explicitly stating, scrutinizing, and regularly updating these underlying assumptions. Sensitivity analysis, which examines how the forecast changes if certain assumptions vary, is a valuable technique to build more resilient and realistic predictions.

Types of Financial Forecasting Methods

Various methods can be employed for financial forecasting, each with its strengths and suitability depending on the data available, the industry, and the purpose of the forecast. These methods broadly fall into two categories: qualitative and quantitative.

Qualitative Forecasting Methods

Qualitative methods are typically used when historical data is scarce or unreliable, or when significant changes are anticipated that historical patterns might not capture. They rely heavily on expert judgment and subjective assessments.

- Delphi Method: This technique involves soliciting opinions from a panel of experts, often anonymously, to arrive at a consensus forecast. Iterative rounds of questioning and feedback help refine the predictions and reduce bias.

- Market Research: Gathering information through surveys, interviews, and focus groups can provide insights into customer preferences, market demand, and competitor strategies, which can then be used to inform sales and revenue forecasts.

- Sales Force Opinion: Salespeople, being on the front lines, often have valuable insights into customer intentions and market trends. Their aggregated opinions can form a basis for sales forecasts, though potential optimism bias needs to be managed.

Quantitative Forecasting Methods

Quantitative methods rely on historical data and mathematical models to predict future outcomes. They are generally preferred when sufficient historical data is available and patterns are expected to continue.

- Time Series Analysis: This involves analyzing historical data points collected over time to identify patterns, trends, seasonality, and cyclical variations.

- Moving Averages: Simple moving average calculates the average of a specific number of past data points to predict the next. Weighted moving average assigns different weights to recent data points.

- Exponential Smoothing: Similar to moving averages but assigns exponentially decreasing weights to older observations. It's particularly useful for data with no clear trend or seasonality.

- ARIMA (AutoRegressive Integrated Moving Average) Models: More sophisticated models that capture complex patterns in time series data, including autoregression (dependence on past values) and moving average components.

- Regression Analysis: This statistical technique examines the relationship between a dependent variable (what you want to forecast, e.g., sales) and one or more independent variables (factors that influence it, e.g., advertising spend, GDP). Simple linear regression involves one independent variable, while multiple regression uses several.

- Econometric Models: These are complex models that integrate economic theories with statistical techniques to forecast macroeconomic variables or their impact on a business. They might incorporate factors like GDP, inflation, interest rates, and unemployment rates.

- Scenario Planning: While not strictly a forecasting method in itself, scenario planning is a powerful technique that uses multiple forecasts. It involves developing several plausible future scenarios (e.g., best-case, worst-case, most-likely) and then forecasting financial outcomes for each scenario. This helps businesses prepare for a range of possibilities and assess risk.

The choice of method often depends on the business context, the availability and quality of data, and the required level of accuracy. Often, a combination of methods provides the most robust and reliable financial forecasts.

Key Components of Effective Financial Forecasting

A truly effective financial forecast isn't just about projecting a single number; it's a holistic view that integrates various financial statements and operational metrics. Several key components must be diligently forecasted and understood to paint a comprehensive picture.

Revenue Forecasting

This is arguably the most critical component, as it underpins all other financial projections. Revenue forecasts estimate future sales based on historical trends, market analysis, pricing strategies, sales pipeline data, and economic outlook. Accurate revenue forecasting is challenging due to external factors like competitor actions, economic downturns, or shifts in consumer behavior, but its precision directly impacts the viability of expense plans and profitability targets.

Expense Forecasting

Forecasting expenses involves predicting future operational costs, categorized into fixed (e.g., rent, salaries, depreciation) and variable (e.g., cost of goods sold, commissions). Accurate expense forecasting is essential for budgeting and controlling costs. It helps identify areas for potential savings and ensures that the business can cover its operational needs. This often involves detailed analysis of historical spending, contractual obligations, and anticipated changes in business activities or input costs.

Cash Flow Forecasting

Perhaps the most vital component for short-term operational stability, cash flow forecasting predicts the inflow and outflow of cash over a specific period. Unlike profit, which can include non-cash items, cash flow tracks actual liquidity. A positive cash flow ensures the business can meet its immediate obligations, pay suppliers, and handle payroll. This forecast typically separates operating, investing, and financing activities, providing insights into the sources and uses of cash. Businesses can be profitable on paper but fail due to poor cash flow, making this forecast indispensable.

Profit and Loss (P&L) Forecasting

Also known as the income statement forecast, this component projects a company's revenues, costs, and ultimately, its net profit or loss over a future period. It integrates revenue and expense forecasts to show the expected profitability of the business. The P&L forecast is crucial for evaluating a company's operational efficiency and its ability to generate earnings, which is a key metric for investors and stakeholders.

Balance Sheet Forecasting

This involves projecting the future state of a company's assets, liabilities, and equity at a specific point in time. It brings together the P&L and cash flow forecasts, as changes in revenue, expenses, and cash directly impact balance sheet accounts like accounts receivable, accounts payable, inventory, and retained earnings. A balanced forecast ensures consistency across all financial statements and provides a comprehensive view of the company's financial position.

Importance of Data Quality and Historical Data

The accuracy of any financial forecast hinges heavily on the quality and relevance of the underlying data. Historical financial statements, sales records, operational metrics, and market data serve as the foundation. Data must be clean, consistent, and granular enough to support meaningful analysis. Inaccurate or incomplete historical data will invariably lead to flawed projections, emphasizing the need for robust data collection and management systems.

The Process of Implementing Financial Forecasting

Implementing an effective financial forecasting process is not a one-time event but an ongoing cycle of planning, execution, and review. A structured approach ensures consistency, accuracy, and relevance.

1. Define Objectives and Scope

Before anything else, clearly articulate what the forecast aims to achieve. Is it for strategic planning, budgeting, liquidity management, or investor relations? Define the forecasting horizon (e.g., 3 months, 1 year, 5 years) and the level of detail required. Different objectives will necessitate different levels of granularity and types of forecasts (e.g., short-term cash flow vs. long-term strategic P&L).

2. Gather Relevant Data

This involves collecting comprehensive historical financial data (sales, expenses, cash flows, balance sheets), operational data (production volumes, customer numbers, inventory levels), and external market data (economic indicators, industry trends, competitor data). Ensure the data is accurate, consistent, and available for the chosen forecasting period.

3. Select Appropriate Forecasting Methods

Based on the objectives, data availability, and the nature of the business, choose the most suitable qualitative and quantitative forecasting methods. For instance, a mature business with stable sales might rely on time series analysis, while a startup might lean on qualitative methods and market research. Often, a combination of methods yields the most robust results.

4. Develop Assumptions

This is a critical, often iterative step. Identify and document all key assumptions that will drive the forecast. These include internal assumptions (e.g., pricing, staffing, CapEx, marketing spend) and external assumptions (e.g., economic growth, inflation, interest rates, competitive landscape). Be transparent about these assumptions, as they significantly influence the forecast's outcome.

5. Build the Financial Models

Translate the chosen methods and assumptions into comprehensive financial models. This typically involves using spreadsheets (like Excel) or specialized financial planning software. The models should integrate revenue, expense, cash flow, and balance sheet projections, ensuring interdependencies are correctly accounted for. Structure the models to be flexible, allowing for easy adjustment of assumptions and scenario analysis.

6. Generate Forecasts and Analyze Results

Run the models to produce the initial financial forecasts. Review the results critically. Do they make sense? Are there any unexpected spikes or dips? Compare them against previous forecasts or industry benchmarks. Perform sensitivity analysis to understand how changes in key assumptions impact the outcomes. This step often involves iteration and refinement.

7. Communicate and Integrate

Present the forecasts to relevant stakeholders (e.g., management, department heads, board members). Clearly explain the underlying assumptions, methodologies, and the implications of the forecasts. Seek feedback and incorporate valid insights. The forecast should then be integrated into the company's budgeting process, operational plans, and strategic decision-making framework.

8. Monitor, Review, and Adjust

Financial forecasting is an ongoing process. Regularly compare actual results against the forecasted figures (variance analysis). Identify the reasons for any significant deviations. This feedback loop is crucial for improving the accuracy of future forecasts. Economic conditions, market dynamics, and internal operations are constantly changing, so forecasts must be reviewed and adjusted periodically (e.g., monthly, quarterly) to remain relevant and reliable.

Leveraging Financial Forecasting for Strategic Decision-Making

The true value of robust financial forecasting lies in its ability to empower strategic decision-making, transforming a business from reactive to proactive. By providing a clear forward-looking view of the company's financial health, it enables leaders to navigate complex challenges and seize opportunities with confidence.

Budgeting and Resource Allocation

Forecasts provide the quantitative basis for annual budgets and ongoing resource allocation. By knowing projected revenues and expenses, businesses can allocate capital and operational budgets effectively across departments, ensuring that resources are directed to areas that will yield the highest return and align with strategic priorities. This prevents overspending in some areas while under-resourcing critical growth initiatives.

Capital Expenditure Decisions

Major investments in property, plant, and equipment (CapEx) require significant capital. Financial forecasts, particularly long-term cash flow and balance sheet projections, help determine if a company has the financial capacity to undertake such investments, when is the optimal time to do so, and what the return on investment might be. This ensures that capital is deployed wisely to fuel growth without jeopardizing liquidity.

Working Capital Management

Cash flow forecasts are indispensable for optimizing working capital. By predicting future cash inflows and outflows, businesses can manage inventory levels, accounts receivable, and accounts payable more effectively. This allows them to minimize idle cash, negotiate better payment terms with suppliers, and ensure sufficient liquidity to meet operational needs, all of which directly impact profitability.

Risk Management and Scenario Planning

Financial forecasts serve as an early warning system for potential financial risks, such as liquidity shortages, declining revenues, or increasing costs. By running multiple scenarios (e.g., best-case, worst-case, most-likely), businesses can assess their vulnerability to various economic conditions or market shocks. This enables the development of contingency plans, such as securing lines of credit or identifying cost-cutting measures, before a crisis hits.

Growth Strategies and Expansion

When considering expansion into new markets, launching new products, or acquiring other businesses, financial forecasts are essential. They help assess the financial viability of such ventures, project potential revenues and costs, and evaluate the impact on the overall financial health of the company. This data-driven approach minimizes risks associated with ambitious growth initiatives.

Investor Relations and Fundraising

For companies seeking external funding, whether from banks, venture capitalists, or public markets, compelling financial forecasts are non-negotiable. Investors and lenders use these projections to evaluate the company's future earnings potential, repayment capacity, and overall financial stability. A well-articulated and defensible forecast can significantly enhance a company's attractiveness to potential funders.

Challenges and Best Practices in Financial Forecasting

While the benefits of financial forecasting are immense, the process is not without its challenges. However, by adhering to best practices, businesses can significantly enhance the accuracy and utility of their forecasts.

Common Challenges

- Volatility and Uncertainty: The modern business environment is characterized by rapid changes in technology, consumer behavior, and economic conditions. This inherent volatility makes long-term forecasting particularly challenging.

- Data Limitations: Inaccurate, incomplete, or inconsistent historical data can severely compromise the reliability of quantitative forecasts. Businesses lacking robust data management systems often struggle here.

- Human Bias: Forecasters, consciously or unconsciously, can introduce bias into predictions. Optimism bias, where forecasts are overly positive, is a common pitfall, especially when forecasts are tied to performance targets.

- Complexity: Building comprehensive financial models that accurately reflect business operations and external factors can be highly complex, requiring specialized skills and significant time investment.

- Lack of Integration: Often, forecasting is done in silos, disconnected from budgeting, strategic planning, or operational teams. This leads to inconsistent numbers and a lack of organizational alignment.

- Over-reliance on Past Trends: Simply extrapolating past trends without considering future market shifts, new technologies, or competitive actions can lead to significantly inaccurate forecasts.

Best Practices for Effective Financial Forecasting

- Embrace Multiple Scenarios: Instead of a single "point estimate," develop best-case, worst-case, and most-likely scenarios. This provides a range of potential outcomes and helps in risk assessment and contingency planning.

- Focus on Key Drivers: Identify the most impactful internal and external drivers of your business performance. Focusing efforts on accurately forecasting these key variables will yield more precise overall forecasts.

- Involve Cross-Functional Teams: Forecasting should not be solely a finance department function. Involve sales, marketing, operations, and HR teams to gather diverse perspectives and ensure that forecasts reflect operational realities and market insights. This also fosters ownership and accountability.

- Regular Review and Adjustment: Forecasts are living documents. Establish a rigorous review cycle (e.g., monthly or quarterly) to compare actual results against predictions. Analyze variances, understand the causes, and update forecasts accordingly. This continuous feedback loop improves accuracy over time.

- Leverage Technology: Utilize specialized financial planning and analysis (FP&A) software, business intelligence (BI) tools, or advanced spreadsheet capabilities. These tools can automate data collection, build more sophisticated models, and facilitate scenario analysis, reducing manual errors and increasing efficiency.

- Document Assumptions Explicitly: Clearly state and regularly review all underlying assumptions. This transparency helps in identifying the sources of forecast deviations and makes the forecast more defensible and understandable to stakeholders.

- Maintain Flexibility: Build models that are adaptable and can be easily modified to incorporate new information, changing market conditions, or revised assumptions without requiring a complete rebuild.

- Understand the "Why": Beyond the numbers, understand the qualitative reasons behind trends and deviations. This deeper insight helps in making better strategic adjustments.

- Keep it Simple (Initially): While sophisticated models are tempting, start with simpler models that capture the core dynamics. Complexity can be added as data quality and understanding improve.

By proactively addressing these challenges and adopting these best practices, businesses can transform financial forecasting from a daunting task into a powerful strategic asset.

Conclusion

In an era defined by rapid change and intense competition, the ability to anticipate future financial performance is no longer a luxury but a fundamental requirement for sustainable growth and profitability. Financial forecasting serves as the compass that guides businesses through uncertain waters, transforming historical data and informed assumptions into a actionable roadmap for the future. From meticulous revenue and expense projections to critical cash flow and balance sheet analyses, a comprehensive forecasting framework provides the clarity needed to make strategic decisions.

By embracing diverse forecasting methodologies, involving cross-functional teams, and committing to continuous review and adjustment, organizations can mitigate risks, optimize resource allocation, and identify pathways to enhanced profitability. The challenges inherent in forecasting—volatility, data limitations, and bias—are formidable, but they are surmountable through disciplined best practices and the judicious use of technology. Ultimately, robust financial forecasting empowers leaders to set realistic goals, manage capital effectively, and confidently pursue growth opportunities, ensuring long-term success and a truly profitable future.